Car finance: Personal Contract Purchase, hire purchase, contract hire and more compared

If you need a new car but don’t want to pay up front, there are many finance options to choose from. We reveal everything you need to know about each, including the pros, cons and costs.

Finding the right car finance

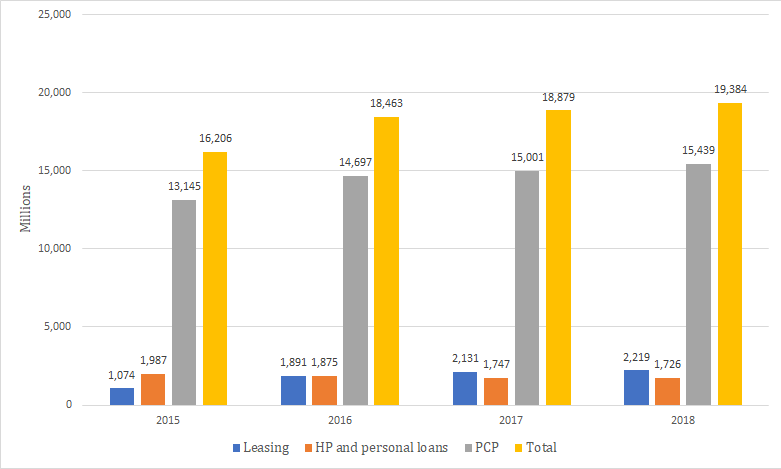

Personal Contract Purchase (PCP) is by far the most popular way to finance new or used cars, according to the latest data available from the Finance & Leasing Association (FLA).

The value of new business via PCP for new cars was approximately £15.4 billion in 2018, significantly higher than leasing (£2.2 billion) and hire purchase (HP) and personal loans at £1.7 billion.

Over the same period, the value of new business via PCP for used cars was £8.9 billion, followed by HP and personal loans at approximately £8.6 billion, while the value of leasing cars stood at £110 million.

Why it’s important to shop around

Before we go through all your different options in detail below to help you decide which is best for you, it’s important to shop around or speak to a broker to find the cheapest price.

After all, there’s no point doing all this research and then getting ripped off on price.

You could use a motoring finance broker such as CarFinance247. By using a specialist broker, you can get a quote for a car finance agreement (without impacting your credit score) and find the right vehicle for your needs.

A broker can be particularly helpful if you have a poor credit rating and have struggled to find a finance agreement elsewhere as they have a panel of lenders that may be willing to help.

You don’t have to pay anything or conduct any checks when using a reputable broker as they will do this for you – plus they might even deliver the car directly to you.

According to carbuyer.co.uk, specialist brokers can knock up to £5,000 off the price of a vehicle (compared to the manufacturer’s original price), but they may not be as flexible as a car dealership.

For example, you may not be able to part exchange your old car and you might not always get a personalised service.

You also need to make sure you use a reputable broker, so be sure to look at previous reviews – and avoid those who ask for money upfront.

Reputable brokerage companies will never charge to source a car as the dealerships they work with will pay them a small percentage fee for introducing the customer, according to Auto Express.

If you're after a new vehicle, it’s also worth checking that if it is actually new! You can do this by checking that your name is the first one on the registration document.

If you’re not keen on using a broker, you could use other sites such as Auto Trader to help you find the best deal on new cars, which also considers your budget, location and length of the contract.

Get breakdown cover from £6 a month with the AA

Your finance options: a quick summary

How a PCP agreement works

With a PCP agreement, you’re effectively renting the car for the duration of the contract with the option of buying it at the end. The lender pays for the car on your behalf, which of course, you’ll need to pay back.

You’ll need to agree with the car dealer the amount you want to borrow, and you’ll have to pay a deposit upfront (usually 10% of the value of the vehicle).

As part of the application process, you'll need to pass a credit check, while the amount that you repay varies, depending on the car and length of the contract.

You’ll pay the full price of the car and interest, while the future value of the car is deferred to the end of the contract – this is known as the Guaranteed Future Value (GFV).

GFV takes into account the condition and age of the vehicle and how many miles it is expected to have covered by the end of the contract.

Unlike buying the car outright, there are certain restrictions to keep an eye out for, especially annual mileage.

It’s vital you don’t exceed any mileage restrictions and avoid any damage to the car in order to prevent any extra charges at the end of the contract. You should ask for examples of what counts as damage or excessive wear and tear.

If you think you may go over the permitted mileage, it might be a good idea to go for a different deal with more mileage on offer.

Once your contract is up, it’s up to you whether you want to return the car, pay the GFV and keep it or trade in the car.

According to the FLA, the most popular option at the end of contract is to start a new PCP agreement.

The last option allows you to use the car’s value (after you pay the GFV) as a deposit on a new PCP agreement.

If you choose to keep the car, you’ll need to make a final payment sometimes known as a ‘balloon payment,’ which is the GFV.

This can vary from a few hundred to several thousand pounds.

How to get the best part-exchange car deal

Lease purchase

A lease purchase agreement is similar to a PCP agreement although you cannot return the car.

You pay a deposit against the car and make monthly payments for the duration of the contract that typically lasts between two and four years.

Unlike a PCP agreement, you must pay the deferred payment to own the car, which is the vehicle’s future resale value.

Several factors, such as the anticipated mileage, age of the vehicle and length of the contract are taken into consideration.

Contract hire

You can use contract hire leasing to fund the use of a car. Over the term of the agreement, you pay the total amount the vehicle depreciates, plus interest and charges.

Before you sign a contract hire agreement, you need to agree on the mileage allowance, which is linked to your monthly payments.

So, a higher mileage allowance will bump up the monthly payments. If you exceed the mileage allowance, you will have to pay extra. According to Financing Your Car, you will have to pay an additional pence per mile charge.

You also need to pay a deposit upfront, which is usually the equivalent of at least three monthly payments.

Once you’ve passed credit and affordability checks, the company pays for the car on your behalf and lends it to you for the set amount of time.

You need to pay the monthly payments and hand in your car at the end of the contract – you don’t have the option to buy the vehicle.

Also, you’ll need to return the car in a good condition with no damage or wear and tear. As we mentioned before, it’s a good idea to check how this is defined in the contract.

Hire purchase

With a hire purchase agreement, you have the option to own the car at the end of an agreement.

While you are technically the registered keeper of the car and you have to insure and maintain it, you won’t own the vehicle until the full amount has been repaid to the finance company.

If you decide to go with a hire purchase agreement, you need to agree on the amount to borrow, which is based on the price of the car.

Similar to other financial products, you need to pay a deposit upfront, which tends to be 10% of the car’s value.

In some cases, you might be able to get a deposit contribution, where the manufacturer offers you money towards your deposit, which will cut the cost of the overall finance agreement.

But you need to make sure that the deal you’re signing up for is right for you, so check the amount of interest you would need to pay, over what term and whether there’s a better deal elsewhere.

Before the contract starts, a fixed APR is set and the loan period is decided, which is often three to four years. As the finance agreement is secured against the car being bought, lenders can be flexible in their terms and conditions.

Once you’ve repaid everything, you can buy the car outright via an ‘option to purchase’ fee, which covers the cost of transferring ownership of the vehicle.

On average, this costs between £100 and £200, but it can vary so it’s best to ask before buying.

Found a car? Check your finance options with CarFinance247

Personal loan

If you don’t have enough money for a deposit and want to own a car outright, you could opt for a personal loan through a specialist broker or via a comparison site.

One of the benefits of using a broker to find a personal loan is that you can benefit from additional services, while a comparison site will only compare different loans on the market.

A potential downside of getting a personal loan is that you won’t have the option to return the car, which is possible under other financing agreements.

So, you’ll need to be confident that you can pay back the loan and any interest on top.

And if you have a bad credit rating, you might not be able to bag one of the best loans available on the market.

Financing Your Car also flags that all of your car’s current market value could be recouped if you sold it or traded it in as a deposit for your next vehicle.

Find the cheapest car loans with loveMONEY

Credit card

A credit card could be used to buy a car outright (if your limit is high enough), but interest rates tend to higher compared to traditional dealer finance options, so this could be a more expensive option.

You should make sure you can pay off the balance in full and make the minimum monthly repayments – even if you’re using a 0% new purchase credit card.

If you don’t have a credit card yet, you should check your chances of approval as a rejected application could harm your credit rating.

Mortgage top-up

You can borrow money from your mortgage provider by withdrawing equity from your home or getting a second-charge mortgage – this is when a borrower’s home is used as security.

If the mortgage provider allows you to borrow money, it will be transferred to your bank account and you repay them according to any pre-arranged terms and conditions.

It’s important to stress your house could be repossessed if you don’t keep up with your regular repayments, so you should make sure you can afford them.

Cheapest car finance option?

The FLA was unable to say exactly which way of financing a car would be the cheapest, as there were too many variables.

This includes the customer’s credit profile, interest rate offered, how much deposit is paid, the agreed mileage per year and the make and model of the car.

So, we used Admiral’s car finance calculator to compare the costs between the most popular methods of financing a car, which are a PCP agreement, HP contract and a personal loan.

These are only indicative costs to give you an idea of what to expect and can vary depending on the type of car you go for.

First, let’s compare the costs of getting a £25,000 car, assuming a 10% deposit (£2,500) has already been paid.

So, in these scenarios, you would be borrowing £22,500 back over nearly four years.

Using PCP, you would pay £416.37 over 47 months at 7.9% APR and a final payment of £7,631 if you want to buy the car.

Admiral bases this final payment on a ‘popular hatchback car with a 1.25 engine and contract mileage of 40,000.’

Overall, excluding your deposit and a part exchange, you would pay £27,200.39 under a PCP agreement.

If you choose a hire purchase agreement, you will pay 47 monthly installments of £545.37 at 7.9% APR and a final payment of £546.37 to own the car.

The overall cost of £26,178.76 (excluding deposit and part exchange) and final payment (£546.37) are both significantly lower than the PCP option.

But on the flip side, the monthly costs under a HP agreement are higher.

If you got a personal loan for £22,500 and had around four years to pay it, your monthly repayments would be £517 at 4% APR (interest rates tend to be lower when someone borrows a larger amount of money).

The overall amount you’ll have to repay would be £24,345 – making it cheaper than both a HP and PCP agreement.

But you should bear in mind that your credit rating affects how much interest you’ll have to pay, so you may end up with a higher or lower rate.

It’s best to compare all your options to figure out the best way to finance your vehicle, but hopefully this has provided some insight on what sorts of costs to expect.

In the next part of our guide, we’ll run through the pros and cons of each way you can finance your car.

Find the right package with CarFinance247

PCP agreement: pros and cons

PCP agreements are ideal for people who prefer to change cars regularly and want lower fixed monthly repayments.

One of the biggest benefits of a PCP agreement is that they are regulated (unless you opt out), so you should have certain legal rights and protections.

You also have the flexibility to choose what you want to do with the car by either choosing the own the car outright, handing it back or trading it in to help buy a new vehicle.

Of course, there are some drawbacks to consider.

As we’ve mentioned before, the ‘balloon payment’ can be several thousands of pounds and you need to stick to the agreed mileage allowance, as well as return the car in a good condition to avoid charges.

While you’re likely to have lower monthly repayments compared to a HP deal, you’ll probably pay more overall, particularly if you use a second finance agreement to pay the deferred future value of the car.

If you want to end your agreement early and return the car, you have this right under the Consumer Credit Act – as long as you’ve already made half your payments.

If you haven’t paid off half the value of the car, you’ll need to pay the difference to end your contract.

Money Advice Service advises anyone to think carefully about whether they are likely to keep the car at the end of the PCP contract.

If not, leasing a car through a contract hire agreement might be the cheaper option.

Balloon finance and payments on your car: how do they work and what will they cost?

Lease purchase: is it right for you?

If you want to finance a more expensive or premium car, a lease purchase agreement, which allows you to choose the length of your deal, might be a good option for you.

You may be able to enjoy lower monthly repayments compared to other financing options as you pay a deposit upfront and a balloon payment at the end of the contract.

The balloon payment is based on the estimated future resale value of the vehicle, so the more it holds its value, the more affordable this type of agreement can be.

Sadly, there are a few disadvantages.

You don’t have the option to return the car, so you should be confident you actually want it – but remember you won’t actually own it until you’ve fully repaid the lender.

On top of this, you need to make sure you have enough money to pay the balloon payment, which must be paid when the agreement ends.

Financing Your Car warns that the value of your final payment may be higher than the actual market value of your car.

If you want to end your lease purchase agreement early, you’ll need to request a settlement fee – this is the amount you have left to pay.

Unfortunately, this is likely to include penalty charges to cover some interest that you would have had to pay under your original contract.

You may be able to sell the car to cover this fee, but you’ll need the lender to agree first.

Alternatively, you can choose to terminate the deal and return the vehicle, but then you’ve potentially spent a lot of money and still have no car.

According to buyacar, if you’ve paid half the amount due under the lease purchase contract, then you’ll owe nothing more if you end your agreement early.

Contract hire: how it works

A contract hire deal is most suitable for people looking for fixed monthly costs without the option to own the car.

It’s also ideal for VAT registered businesses or sole traders as they can claim back the VAT due on the monthly rental payments, which can incorporate road tax, servicing and maintenance plans.

As you’re only making payments based on how much the car is expected to depreciate plus interest and charges, you may benefit from lower monthly payments compared to other financing options.

You’ll also benefit from certain legal rights and protections, unless you opt out or are a business, according to Financing Your Car.

But you can be hit by charges if you exceed your mileage allowance or the car is damaged beyond ‘reasonable wear and tear.’

You can also be hit with early termination charges if you terminate your contract hire agreement early.

Compare car insurance quotes at Confused.com

Hire purchase: pros and cons

Hire purchase is suitable for people looking for a simple finance agreement with fixed repayments and the option to own the car.

A conditional sale is the same as hire purchase, but you automatically own the car at the end of the contract.

Hire purchase agreements are available in most car dealerships.

As this type of credit agreement is regulated, you have some legal rights and protections and if you’ve paid off half the cost of the car, you can return it and stop the payments.

But you have to make sure the finance company is aware you’re terminating the contract early and returning the car to avoid it looking like you’re defaulting on your payments.

How to improve your credit rating and get the best deals

You’ll have some flexibility when choosing your payment terms and can choose fixed payments, plus you won’t need to stump up a lot of money for a final payment.

Unlike other financing options, hire purchase agreements tend to not have mileage restrictions.

But there are downsides – you won’t own the car until you’ve made the final payment, so if you struggle to pay, your vehicle could be taken away.

Hire purchase can also be an expensive option as the deposit and length term will impact how much you pay each month.

Personal loan: is it right for you?

Personal loans are ideal for people who want to own their car outright but don’t have a deposit. It’s a good idea to shop around for the best deal and figure out how much you can afford to borrow before taking out a loan.

As a personal loan can affect your credit rating, you should use eligibility calculators that use a ‘soft’ search instead of a ‘hard’ one.

It’s also advisable to check how long it would take to pay off a loan and how much needs to be repaid by using a loan calculator.

One of the benefits of using a personal loan is that it’s easy to arrange and you may be able to access lower interest rates – if you have a good credit rating.

As only 51% of those accepted for a credit deal get the advertised rate, it’s not guaranteed that everyone will get the rate they want.

There are other things to consider. Personal loans have a 14-day cooling off period, which means you have two weeks to decide whether the loan is right for you – and you can cancel it.

If you cancel within this period, you’ll still need to pay the capital and interest over the time period within 30 days. Cancelling the loan doesn’t affect the agreement to buy a car from a dealership.

You need to be careful when picking a personal loan as some may offer a variable interest rate where the amount you pay can go up or down.

You can also choose how long you want to pay back the loan although it’s vital to remember the longer the term, the more you’ll have to fork out in interest.

Similar to other financing options, you can choose to settle your loan early by writing to your lender and asking for a settlement amount, which you’ll have 28 days to pay. You should get a rebate on any future interest or charges you have paid.

Alternatively, you can partially settle your loan to make the overall payment smaller (and you’ll receive some rebate).

Credit card: pros and cons

If you have some cash, or the car you want isn't too expensive, you could use a purchase credit card to help fund your purchase.

The best 0% purchase credit cards offer in excess of two years interest-free, so you have a fair while to clear the debt before the hefty interest rates kick in (usually around 20%).

What's more, some may offer rewards when you spend with them and you can also get extra buyer protection under Section 75 of the Consumer Credit Act.

Unfortunately, not all dealerships will accept a credit card or may not let you pay the full amount with one, so you might need to borrow money from elsewhere to pay the remaining amount.

It’s worth mentioning that you may not qualify for a credit card offering 0% interest or you might not get a big enough credit limit to buy a car.

Using a mortgage top-up

A mortgage top-up can be useful for people who want to keep their car for a long time and want to spread the cost over more than four years (the typical time period for a dealer finance agreement).

While the monthly repayments can be more affordable and you have more breathing room to pay back the money, you may end up inadvertently end up paying a lot more in interest.

This also means that the cost of buying a car is actually a lot higher compared to other financing methods.

We’ve mentioned this before but it’s worth reiterating.

You could risk your house getting repossessed if you don’t keep up with the regular payments, so you should carefully consider whether you can afford to use a mortgage top-up.

Money Advice Service says if you’re wanting to pay for something expensive (other than home improvements or investment property), you should consider options where the loan is not secured against your home.

Why mortgage lenders turn you down

Buying with cash

If you’re planning to buy outright with cash, just make sure you have enough left over to keep your emergency savings pot topped up.

And, as mentioned earlier, you might also want to consider paying just £100 of the cost of the car on a credit card as this means the card company and retailer are jointly liable if something goes wrong under Section 75 of the Consumer Credit Act.

The best time to buy a car

You may be able to get a better deal by buying a car at certain times of the year.

The end of June and December may be ideal as dealers want to shift cars to help them hit their quarterly targets, according to the Money Advice Service.

If you’re not bothered about your number plate, dealers want to get rid of used cars with older plates in February or August so you could bag a handy discount.

Be aware when certain types of cars will be in demand, which could push prices higher. So, as an obvious example, sports cars will be in higher demand in the summer while four-wheel drive cars may be highly sought-after over winter.

By buying outside of periods of high demand for certain cars, you could save more.

Check your finance options with CarFinance247

Selling your old car: best options

Unless you're going down the part exchange route or buying an additional car, you'll also need to get rid of your old wheels.

As with car finance, there are loads of different options to choose from. Some are really straightforward but might not get you a great price, while others will take time and effort but ensure you are better rewarded as a result.

So which option should you go for? Our complete guide to selling your car runs through all your options including what to expect, fees and more.

*This article contains affiliate links, which means we may receive a commission on any sales of products or services we write about. This article was written completely independently.

Comments

Be the first to comment

Do you want to comment on this article? You need to be signed in for this feature