MPs: State Pension triple lock 'should be scrapped’

A Government committee is calling for the 2.5% benchmark to be removed to protect future generations.

The State Pension triple lock should be scrapped, according to a new report by the Commons Work and Pensions Committee that looks into intergenerational fairness.

The triple lock ensures the amount of State Pension people receive rises each year by the highest of inflation, earnings growth or 2.5%.

The mechanism devised by the Liberal Democrats and implemented by the Coalition Government in 2012 was brought in to help improve pensioner incomes.

It has helped raised the basic State Pension from £102.15 a week in April 2011 to £119.30 a week today – meaning pensioners are earning £891.80 a year more and the system will also apply to the new State Pension introduced earlier this year.

However, the guarantee is expected to cost an extra £4.5 billion a year over the next five years and the committee warn the retention of the mechanism would lead to State Pension expenditure accounting for an even great share of national income.

MP Frank Field, who is chairman of the cross-party committee, said: "Each generation is supported in retirement by their in-work successors. This is supported by all age groups, but a combination of factors has sent the balance out of kilter.

"It is now the working young and their children who face the daunting challenge of getting on in an economy skewed against them."

Plan for your future: visit the loveMONEY investment centre today

New plan

The committee say the three benchmark guarantees from the triple lock are unsustainable and other solutions like increasing the State Pension age aren’t viable.

Instead it's proposing replacing the triple lock in 2020 with a system that ensures the weekly payment is linked to earnings with a temporary switch to inflation when it exceeds wage growth.

The report explains: “In periods when earnings lag behind price inflation, an above-earnings increase should be applied to protect pensioners against a reduction in the purchasing power of their State Pension.

"Price indexation should continue when real earnings growth resumes until the State Pension reverts to its benchmark proportion of average earnings."

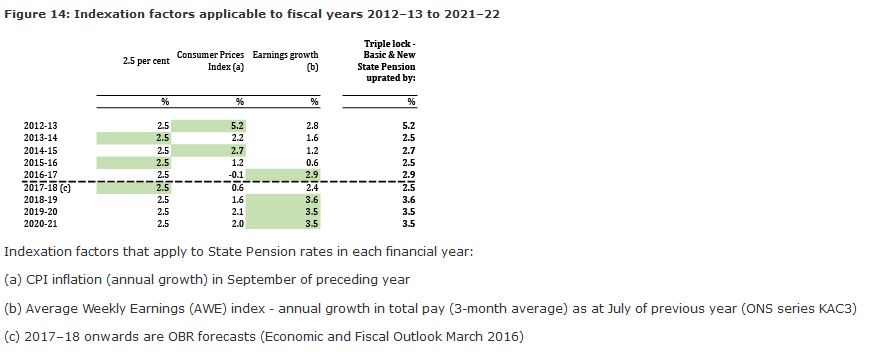

The new system will ensure pensioner incomes still rise but crucially the 2.5% benchmark will disappear. Over the last four years the 2.5% benchmark has uprated pensions twice (in 2013 and 2015) – when inflation and earnings were at rock bottom.

However, some have called the benchmark ‘arbitrary’ and claimed that, based on Office for Budget Responsibility predictions, will soon become obsolete as earnings growth rises.

The table below sets out how the triple lock has worked so far and how it may become less important going forward.

The new proposal is "fiscally sustainable (unlike a simple double lock, which would mean the value of the State Pension continuing to grow relative to the rewards of work, especially during times of economic difficulty) but fulfils the objectives of supporting pensioners who would share in the proceeds of growth and get protection against high inflation," the committee says.

Frank Field added: "The system we propose protects pensioners and allows them to share the proceeds of future good times, but at the same time is inter-generationally fair.

"We call on all parties to get behind it.”

Pensioner poverty

Experts laud the triple lock as a tool that has helped bring pensioner incomes back into line with the rest of the population. It’s feared the end of the triple lock could mean more pensioners struggling to get by.

Tom McPhail, head of retirement policy at investment firm Hargreaves Lansdown, warns this could become a reality – especially with other pension shifts on the horizon .

"It is also important to recognise that pensioner incomes will change again in the future... successive pensioners will be increasingly reliant on the State Pension and on defined contribution arrangements.

"Any measure to curb either of these in the next few years could rapidly push more pensioners back into poverty.”

Interested in a SIPP or stocks and shares ISA? Visit the loveMONEY investment centre today

More from loveMONEY:

Deferring your State Pension: how much can you get and is it worth it?