Annuity rates cut 23 times since July!

Pension incomes have taken a hit in the last two months with annuity providers slashing rates on 23 occasions!

When we retire, many of us will want to cash our retirement pot in for an annuity. You basically hand over your savings to an insurer, which promises to provide you with an income for the rest of your life.

Unfortunately, the annuity rates on offer have been falling for a while now. But according to broker Hargreaves Lansdown, the market-leading rate has been cut an incredible 23 times since the beginning of July. That’s 14 cuts in July and a further nine this month.

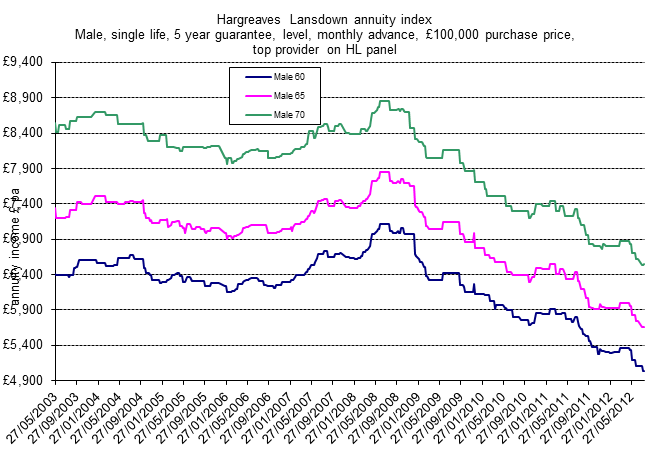

The graph below tracks how the top annuity rate on offer has changed since 2003, putting the current record low rates on offer in grim context.

As if that isn’t bad enough, Hargreaves Lansdown has forecast further falls this year. There are four main reasons for this:

More extensive use of underwriting

The figures above track standard annuity rates. But not everyone gets standard annuities – some qualify for impaired annuities. This is where you have some sort of condition or medical history which makes it likely that you won’t live as long. As a result you’ll get a better annuity.

But if you underwrite everyone, and move the unhealthy over to enhanced annuities and offer them higher rates, standard annuity rates will inevitably have to be cut.

Improving life expectancy

In 2010 average life expectancy for both men and women in the UK rose. For newborns, men will now on average reach 78.2 years while women will hit 82.3 years. Meanwhile, for those at age 65, age expectancy grew by two months.

The longer that an insurer thinks you will live, the lower they will want to shell out on the annuity as they will be stuck paying it for longer.

Solvency 2

Solvency 2 is a new European directive which would force insurers to hold more cash in reserve and invest in more lower-yielding assets. As a result, the returns on those investments will fall, and this will be passed on in the form of lower annuities.

According to Deloitte, Solvency 2 could force annuity rates down by a further 20%.

The Gender Directive

At the end of this year the European Court of Justice’s Gender Directive will come into force. This piece of legislation bans insurers from taking gender into account when working out things like car insurance, life insurance and – you guessed it – annuities.

And that means men will suffer as the (relative) advantage of a lower life expectancy will be eliminated.

What about Quantitative Easing?

The elephant in the room is the Bank of England’s Quantitative Easing (QE) programme. In an attempt to boost the economy, the Bank of England essentially created £375 billion in new money which it used to buy up Government bonds (also known as gilts).

The problem is that this has pushed down the yield on those gilts. Gilt yields are used to calculate pension scheme liabilities. And if the yields are low, pension funds then need more assets to pay sufficient incomes to future pensioners. In other words, pension funds fall into deficit.

Back in March the National Association of Pension Funds said QE had ‘blown a hole’ in pensions, turning a £22 billion surplus among the UK’s final salary pension schemes into a £255 billion deficit.

However, a new report from the Bank of England claims that QE has had a “broadly neutral impact” on annuities. While the Bank admits that QE has pushed down annuity rates, it argues that QE has pushed up the value of assets held by pension funds. In other words, the size of our pension pots has been boosted. So while annuity rates have fallen, it shouldn’t damage the income you can buy with an annuity.

Picking the right annuity

Perhaps the Bank is right. Perhaps not. But what’s not in doubt is that we all need to put in the effort to get the absolute best annuity we possibly can. As we highlighted last month, there can be a 12% difference in income between the top and fifth best annuities.

For a full guide on making the most of your pension pot, check out How to buy the right annuity. And remember you can compare annuities using our annuity calculator.

More on pensions

Cut the cost of passing on your pension

Why young people MUST opt in to auto enrolment

Annuity meltdown will eventually end